Modern family life now runs through screens, apps, cloud accounts, shared subscriptions, online banking, password managers, photos, videos, and digital paperwork. Yet many estate plans still focus mainly on property, savings, and physical documents. That leaves a quiet but serious gap. When a partner, child, parent, or trusted adviser needs access to essential information, the practical problem is often not ownership, it is access.

Digital asset planning solves that problem. It helps families organise what exists, decide what should happen to it, and make sure the right people can access the right information at the right time, without exposing everything to unnecessary risk.

For UK households, this is becoming more important, not less. The Property (Digital Assets etc) Act 2025 has strengthened the legal recognition of digital assets as property in the right contexts, but legal recognition alone does not make passwords retrievable, cloud storage discoverable, or platform rules easier to navigate. Families still need a practical system.

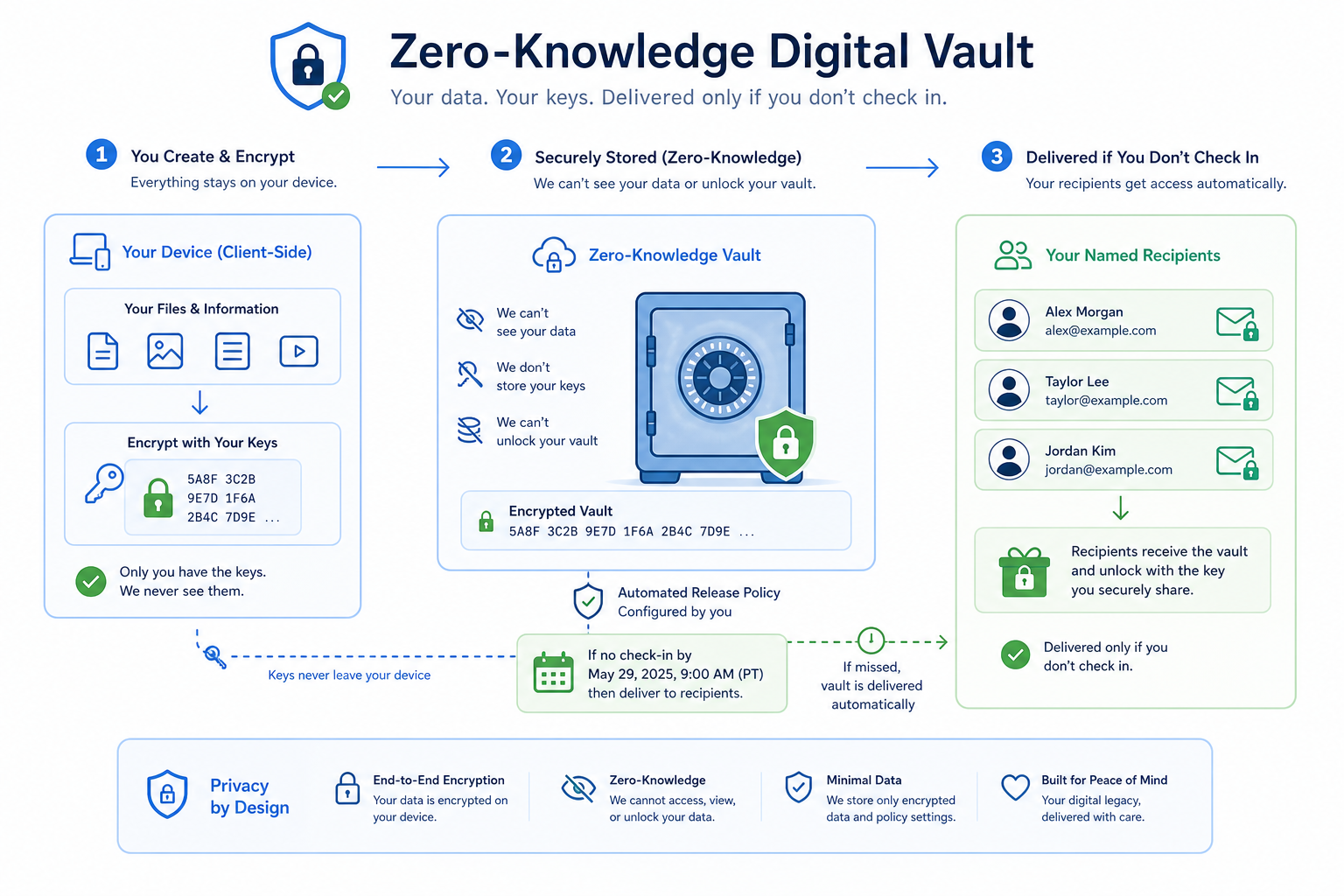

Holdfast was built for exactly this challenge. It is a zero-knowledge digital estate vault with a dead man's switch. Vault contents are encrypted client-side using AES-256, only the intended recipients receive the items assigned to them, and automated delivery only happens after multiple missed check-ins and an escalation process. That means sensitive information stays private while you are managing it, and accessible when your loved ones or professional advisers genuinely need it.

"In the UK, 75% of respondents acknowledged reusing credentials at least some of the time." - IBM

"The global average cost of a data breach is $4.4 million." - IBM

Why digital asset planning matters now

Most people already know they should have a will. Fewer realise they also need a map of their digital life.

That digital life often includes:

online current and savings accounts

investment platforms

payment apps

cryptocurrency and wallet recovery details

shared family photo libraries

email accounts

cloud storage

mobile contracts and utilities

subscription services

online shopping accounts

social media profiles

business tools and domain names

passwords, passkeys, and two-factor recovery methods

letters, wishes, and private messages intended for loved ones

If these are not organised in advance, the result is rarely smooth. Families can spend weeks or months trying to identify what exists, who should handle it, and whether access is even possible. In emotional situations, that uncertainty becomes a burden.

This is why digital legacy planning is not only about wealth. It is also about clarity, privacy, and reducing stress for the people left to manage practical tasks.

What counts as a digital asset

A digital asset is any digitally stored account, record, credential, file, subscription, or item of value, whether financial, practical, or sentimental.

Financial digital assets

These are the most obvious and often the most urgent:

online banking access

investment platforms

pension portals

crypto exchanges and wallets

online payment services

reward balances and valuable digital holdings

Administrative digital assets

These keep daily life running:

email accounts

mobile and broadband accounts

online council tax or utility logins

insurance portals

cloud document storage

password managers

identity verification apps

subscription services

Personal and sentimental digital assets

These are often overlooked, despite having deep value to families:

family photos and videos in cloud storage

voice notes and personal recordings

private letters and messages

social media profiles

memorial pages or personal websites

digital journals and creative work

Business and professional digital assets

For business owners, freelancers, and advisers, the list can extend further:

domain names

company social channels

website hosting logins

invoicing platforms

client records

secure notes

software licences

The legal picture in the UK

Digital asset planning sits at the intersection of estate administration, privacy, contract law, platform rules, and practical access control.

The Property (Digital Assets etc) Act 2025

The Property (Digital Assets etc) Act 2025 is important because it helps confirm that certain digital assets can be recognised as property. That matters for succession, probate, and estate administration.

However, legal recognition is only part of the picture.

A digital asset may be capable of passing through an estate, but that does not mean:

relatives know it exists

executors can find it

passwords or recovery methods are available

platform terms allow transfer

important instructions are documented clearly

The law helps answer whether something can form part of an estate. Good planning answers how anyone will actually locate and manage it.

Probate, executors, and Letters of Administration

In the UK, digital assets may need to be handled by:

executors named in a will

administrators acting under Letters of Administration where there is no valid will

attorneys acting under a Lasting Power of Attorney for property and financial affairs during incapacity, if appropriate

That means your digital planning should not sit in isolation. It should support the wider legal framework that applies to your affairs.

Platform terms still matter

Even where the law recognises digital assets, individual platforms set their own terms for:

memorialisation

account closure

transfer restrictions

access by authorised persons

download rights

inactivity handling

Apple, Google, Meta, LinkedIn, crypto exchanges, and subscription services all have different rules. Some allow designated legacy contacts or inactivity settings. Others permit deactivation but not transfer. Some content is licensed, not owned, which changes what can be passed on.

This is one of the biggest content gaps in many articles on the subject. They explain that digital assets matter, but not that access often depends on a mix of legal authority, technical preparation, and platform-specific settings.

The real risks of poor preparation

Poor digital planning creates more than inconvenience.

1. Important assets are missed

If nobody knows an account exists, it may never be identified. That includes dormant investment accounts, crypto holdings, premium subscriptions, cloud archives, or income-generating digital property.

2. Password inheritance becomes chaotic

Many families still rely on handwritten lists, spreadsheets, shared notes apps, or ad hoc messages. These approaches are fragile, insecure, and difficult to keep current.

3. Sensitive information is overshared

A common mistake is giving one person access to everything. In practice, that is rarely appropriate. Your partner may need household financial information, your solicitor may need legal documents, and your children may only need personal letters or photo access.

4. Sentimental content is lost

Family photos, voice notes, message archives, and private reflections often matter more than money, yet they are frequently left trapped inside phones or cloud accounts.

5. Cybersecurity risks increase

Scattered credentials, password reuse, and unsecured storage methods expose families to fraud precisely when they are least prepared to manage it.

6. Professional advisers face delays

Solicitors, IFAs, accountants, and international legal or financial counterparts can only work efficiently if core information is available and organised. Missing logins, undocumented accounts, and unclear wishes slow everything down.

Why traditional estate planning is not enough on its own

A will is essential, but it is not designed to function as a live operating manual for your digital life.

A will is not a password vault

Including passwords directly in a will is usually a poor idea. Wills become part of the administration process and may be copied, stored, or handled by multiple parties. Passwords also change often, which makes a static legal document impractical.

A will cannot keep pace with digital change

You might open new accounts, change two-factor authentication, move photos to new services, sell crypto, or update recipients. A digital plan needs to be easy to maintain.

Not every recipient should see everything

Traditional estate documentation does not always provide the granularity families need. Digital planning often requires item-by-item sharing rules.

The modern family challenge, ownership versus access

This is the core issue most families face.

You may have every intention of sharing important details with the right people, but when the moment comes, you may no longer be in a position to hand over credentials, explain what matters, or clarify what should happen next.

That is the access problem.

The best digital estate systems solve it by answering five practical questions:

Question | Why it matters |

|---|---|

What exists? | Families and advisers cannot manage what they cannot find |

Where is it? | Cloud, app, device, paper records, password manager, exchange, solicitor |

Who should receive it? | Different people need different information |

When should they receive it? | Immediately, only after escalation, or only if needed |

How will it be delivered securely? | Loose documents and shared notes are not enough |

How Holdfast solves the access problem

Holdfast is designed around privacy, practical delivery, and peace of mind.

Zero-knowledge digital estate vault

Holdfast stores sensitive digital estate information in a zero-knowledge vault. That means the contents are encrypted client-side using AES-256 before storage, so Holdfast cannot read the plaintext contents.

This is especially important for:

credentials

financial details

legal information

private letters

family instructions

video messages

personal records

Controlled sharing by recipient

Not every person needs the same information. Holdfast lets you assign specific items to specific recipients, so each person only sees what they are meant to see.

For example:

a spouse can receive household account instructions

an adult child can receive family photo archive guidance

a solicitor can receive legal contacts and document notes

an IFA can receive relevant financial summaries

a close friend can receive a personal letter or video message

Automated delivery after multiple missed check-ins

Holdfast includes a dead man's switch mechanism. Users complete simple periodic check-ins. If multiple check-ins are missed, Holdfast follows an escalation process before releasing the designated vault contents to nominated recipients.

This matters because the problem is rarely storage alone. It is timing. The information must remain private unless and until it is genuinely needed.

No recipient account required in advance

Recipients do not need a Holdfast account before information is sent. That removes friction and makes planning more realistic for families who are not all equally technical.

Calm, low-maintenance setup

Once configured, the system is simple to maintain. You can update records over time, choose monthly or flexible check-ins, and keep the process light-touch rather than burdensome.

What to include in a strong digital asset plan

A complete plan should be practical, current, and easy for the right people to use.

Core account inventory

Start with a structured list of:

financial platforms

email accounts

cloud storage providers

telecoms and utilities

insurance portals

subscriptions

social media accounts

shopping accounts

crypto holdings

websites and domain names

Credential and recovery planning

You do not necessarily want passwords inside a paper document. But you do need a secure route to access.

Include:

account names and purpose

login identifiers

where credentials are stored

recovery email or phone details

two-factor authentication notes

device dependencies

backup code location

Wishes and handling instructions

For each account or category, decide:

who should access it

whether it should be closed, archived, memorialised, or maintained

whether content should be downloaded

whether any messages or files should be passed to family

whether a professional adviser should be involved

Legal and professional contact details

Include:

solicitor details

will storage details

LPA information

accountant details

IFA or wealth adviser details

business continuity contacts where relevant

Personal letters and messages

A digital plan should not be purely administrative. It can also carry the human side of legacy planning, including:

personal letters

instructions for family milestones

private recordings

video messages

practical notes that reduce stress for loved ones

A practical framework for families

The easiest way to organise a digital estate is to divide it into four layers.

Layer 1, Essential access

These are the items your closest recipient may need quickly:

primary email

mobile account

banking overview

password manager instructions

device unlock guidance

solicitor and adviser contacts

Layer 2, Estate administration support

These help executors or administrators do their work:

asset inventory

account list

document locations

subscriptions to cancel

digital business interests

crypto instructions

tax-related records

Layer 3, Family continuity

These help the household keep functioning:

bills and utilities

household service logins

insurance details

child-related subscriptions or services

shared calendars and file storage

Layer 4, Personal legacy

These preserve meaning, not just logistics:

photos and videos

letters

life notes

values statements

guidance for sentimental digital possessions

Common mistakes to avoid

Relying on memory

Even organised people forget accounts over time.

Storing everything in one unencrypted document

This creates a single point of failure.

Sharing all credentials with one person

This creates privacy, security, and relationship problems.

Ignoring two-factor authentication

Passwords alone are often not enough.

Forgetting platform-specific settings

Legacy contacts, inactivity managers, and memorialisation settings should align with your plan.

Failing to update after life changes

Marriage, separation, children, relocation, new accounts, adviser changes, and business changes all affect digital planning.

Digital asset planning for couples

Couples often assume they already share enough information. In practice, they usually share fragments.

A better approach is to separate:

jointly managed household information

individually private information

legally relevant information

sentimental content intended for later delivery

Holdfast is particularly well suited to couples because it supports controlled sharing without forcing total transparency. One partner can make sure the other receives what is needed, without exposing every private note, account, or message while everything is operating normally.

Digital asset planning for parents and adult children

Parents may want to ensure adult children can help with practical administration, but only in limited ways.

Examples include:

giving one child access to document locations

giving another access to family photos

reserving financial summaries for the executor or adviser

sharing personal messages separately from financial instructions

This avoids both confusion and oversharing.

International families and cross-border considerations

Many families now live internationally, hold accounts across jurisdictions, or use global digital platforms. This makes digital planning more important.

Cross-border complexity can involve:

assets in multiple currencies

global cloud services

international beneficiaries

different privacy rules

varied succession procedures

local platform restrictions

Holdfast is built in the UK and used worldwide. It is compliant with UK GDPR, which the EU recognises as providing an equivalent level of protection - users worldwide are welcome, and data is processed to those standards regardless of where you are based.

That combination of UK data standards and international usability makes it a strong fit for globally connected families and internationally active advisers.

A better security model for digital inheritance planning in the UK

Security matters because digital estate planning contains some of your most sensitive information.

Why zero-knowledge matters

A standard storage service may encrypt data in transit and at rest, but still allow the provider to access content internally. A zero-knowledge architecture is different. If the system is designed properly, the provider cannot read your vault contents.

For digital inheritance planning, that is a major advantage.

Why client-side encryption matters

Client-side AES-256 encryption means data is encrypted before it leaves your device. This reduces exposure and supports a privacy-first model.

Why controlled disclosure matters

Traditional approaches often expose too much, too soon. Controlled sharing means each recipient only receives the information allocated to them.

Holdfast compared with common alternatives

Approach | Strengths | Weaknesses |

|---|---|---|

Paper list in a drawer | Simple to start | Easy to lose, hard to update, insecure |

Spreadsheet of passwords | Familiar | High risk if copied or emailed |

Shared note on a phone | Convenient | Weak access control, device dependent |

Password manager emergency access | Useful for credentials | Limited for letters, wishes, adviser instructions, selective legacy sharing |

Will only | Legally important | Not built for live credential management or practical delivery |

Holdfast | Zero-knowledge storage, client-side AES-256 encryption, recipient-specific sharing, automated delivery, supports documents, credentials, letters, and video messages | Requires initial setup, like any proper planning system |

For solicitors, IFAs, and international professional advisers

Professional advisers are increasingly asked practical questions about digital assets, not just legal theory.

Clients want help with:

organising online account information

planning password inheritance responsibly

protecting confidentiality

reducing burden on family

making instructions discoverable

coordinating legal and practical planning

Holdfast offers a Firm plan designed for legal and financial professionals who want a modern, secure solution they can recommend or manage for clients. It is suitable not only for UK solicitors and IFAs, but also for international counterparts in legal and financial services who need a privacy-focused digital estate planning tool.

This is particularly useful where advisers want to support clients without holding excessive sensitive credential data themselves.

A simple step-by-step process to organise your digital legacy

1. List your digital assets

Make a full inventory across finance, admin, sentimental, and business categories.

2. Decide what each person needs

Think in terms of recipients, not just accounts.

3. Separate access from visibility

Not everyone should receive everything.

4. Record instructions clearly

Explain what exists, what matters, and what should happen.

5. Align with your will and legal documents

Make sure your executors, attorneys, and professional advisers know a digital plan exists.

6. Use secure storage

Choose a platform built for sensitive information, not a workaround.

7. Set a review rhythm

Review after major life changes and at least annually.

Why modern families are moving towards low-maintenance digital planning

The best systems are the ones people actually keep up to date.

Families are busy. They need something that is:

simple to set up

secure by design

easy to revise

clear for recipients

not dependent on memory

not burdensome month to month

That is why low-maintenance check-ins matter. They keep the plan active without turning it into an administrative project.

Final thoughts

Digital asset planning is no longer a niche exercise for highly technical households. It is part of responsible estate planning in the modern world.

The legal landscape is catching up, particularly in the UK, with the Property (Digital Assets etc) Act 2025 reinforcing the importance of digital property. But the family challenge remains practical. Loved ones and advisers need a secure way to locate information, understand your wishes, and receive only what they need, when they need it.

That is where Holdfast stands apart.

It combines zero-knowledge architecture, client-side AES-256 encryption, controlled recipient-by-recipient sharing, automated delivery after multiple missed check-ins, and a calm, dependable user experience. It supports credentials, documents, letters, legal details, and video messages. It is suitable for individuals, couples, families, and professional advisers. It is built in the UK, hosted in the EU (West EU, Ireland) under UK GDPR, which the EU recognises as providing an equivalent level of protection - users worldwide are welcome, and data is processed to those standards regardless of where you are based.

If you want to organise your digital legacy once, properly, and give your loved ones real peace of mind, Holdfast is a practical place to start.

Start with a secure plan, not a patchwork fix

If your current plan relies on memory, paper notes, or hoping someone can work things out later, it is time for something stronger.

Holdfast offers:

Free

Personal, £5/month or £45/year

Family, £9/month or £79/year

Firm, £39/month or £399/year

For modern families, the goal is simple. Keep sensitive information private now, make essential information available later, and remove avoidable stress for the people who matter most.

That is what good digital estate planning should do. That is what Holdfast is built for.